Also, for each time we move from left to right, we must divide the length by 10. This table provides a summary of the Length or Distance units within their respective measurement systems. Volume is measured in millilitres (ml) and litres (l). The metric system is used to measure the length, weight or volume of an object.

Examples of millimeter in a Sentence

Length is measured in millimetres (mm), centimetres (cm), metres (m) or kilometres (km). To measure in mm, hold a metric ruler against an object, count the number of whole cm of its length, and multiply by 10. In case mm meaning you are wondering how to measure length in millimeters or how a length of a millimeter or 1 mm looks like, let’s check it out on a ruler. Some examples of objects having about 1 millimeter length areA sharp pencil point and the tip of a sewing needle are approximately 1 mm in length. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online.

Millimeter Examples

Let us learn more about this metric unit, Bookkeeping for Chiropractors the conversions, and solve a few examples to understand the concept better. The term mm is a popular slang term frequently used in online chat and text conversations. When someone asks you to do something and you don’t want to comply, you can respond with mm to express your refusal.

- A millimeter is usually the smallest unit you can measure using a regular ruler.

- On Twitter, it can be used to recommend a song or music that you believe others should listen to.

- The metric unit consists of meters, centimeters, millimeters, and inches.

- The base unit for a millimeter is meter and the prefix is milli.

- The word is usually expressed as ‘mm’ and is considered to be equal to one-thousandth of a meter.

- This phrase originated from Wiccan witches and is often used in online chatrooms or text messages.

- Here’s a fun example to understand why small units are important.

Articles Related to millimeter

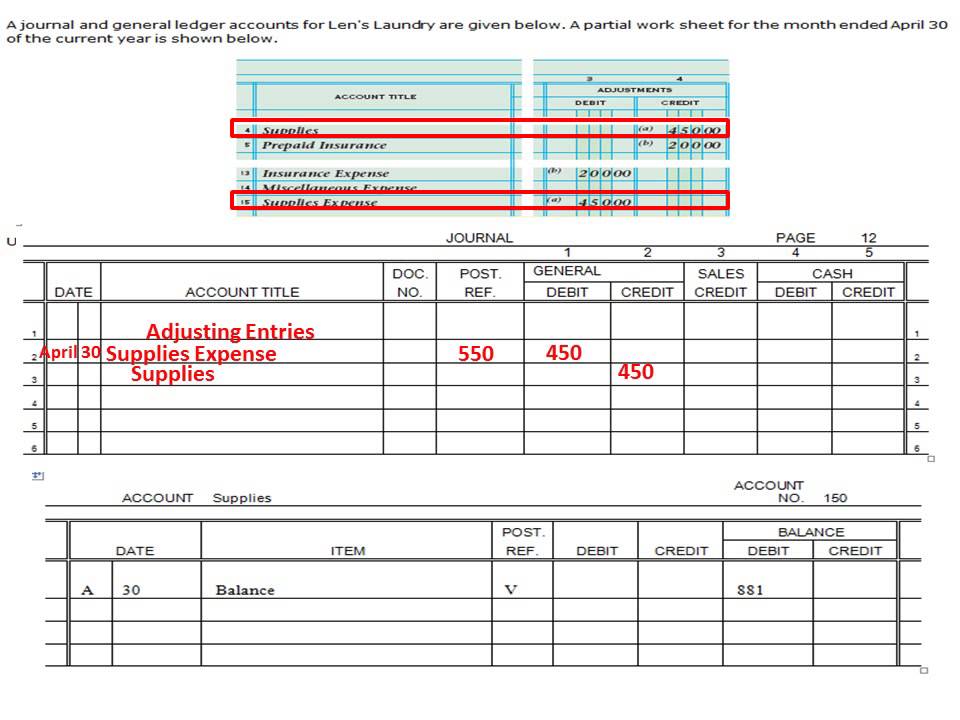

It’s important to note that the meaning of mm from a girl is not significantly different from how everyone else uses it. It is primarily used to express agreement, refusal, recommendation, or as a greeting in pagan culture. If you’re unsure about the specific meaning in a conversation, it’s always best to ask for clarification. As we can see in the chart, from mm to cm, only one jump ledger account to the left is required.

Using a Metric Ruler

The term “mm” is a popular slang term frequently used in online chat and text conversations. It is commonly used as a response to indicate agreement or understanding. When someone asks you to do something and you don’t want to comply, you can respond with “mm” to express your refusal. On Twitter, it can be used to recommend a song or music that you believe others should listen to.

Millimeters (mm) – Length / Distance Conversions

A millimeter can be defined as a metric unit used to measure the length of small or tiny objects such as measuring lines, the length of a pencil tip, etc. The word is usually expressed as ‘mm’ and is considered to be equal to one-thousandth of a meter. The metric unit consists of meters, centimeters, millimeters, and inches. Look at the image of a ruler below, the longer lines with numbers written below them indicate the value of centimeters and the smaller lines indicates the value of millimeter. Millimeter is the metric unit of length used for measuring small objects and quantities such as medicines, length of a pen tip, etc. While measuring the length of any object, meter, centimeter, millimeter, and inch are used.

- Look at the image of a ruler below, the longer lines with numbers written below them indicate the value of centimeters and the smaller lines indicates the value of millimeter.

- While measuring the length of any object, meter, centimeter, millimeter, and inch are used.

- The origin of the word “mm” or its derivation is not clear.

- Can you imagine measuring tiny things using units like yards or miles?

- When someone asks you to do something and you don’t want to comply, you can respond with mm to express your refusal.

Can you imagine measuring tiny things using units like yards or miles? These slang terms serve as concise responses to express various forms of acknowledgement or disagreement, just like “mm” is used to indicate agreement or understanding. We have measures like meters and kilometers to express bigger distances, like the distance between two cities, the height of mountains, lengths of rivers, etc.

.jpg)

.jpg)